Five years ago, we started working on the development of an ambitious pathway for enabling transport to contribute to EU’s climate neutrality ambition by 2050, based on scale up of low-carbon-liquid fuels supply and use, across several transport sectors.

The ambition of the European Union is to be climate neutral by 2050. The European refining industry supports the same ambition.

Our industry is transforming, and we have developed a comprehensive potential pathway of how we, together with our partners, can contribute to meeting the 2050 climate neutrality challenge.

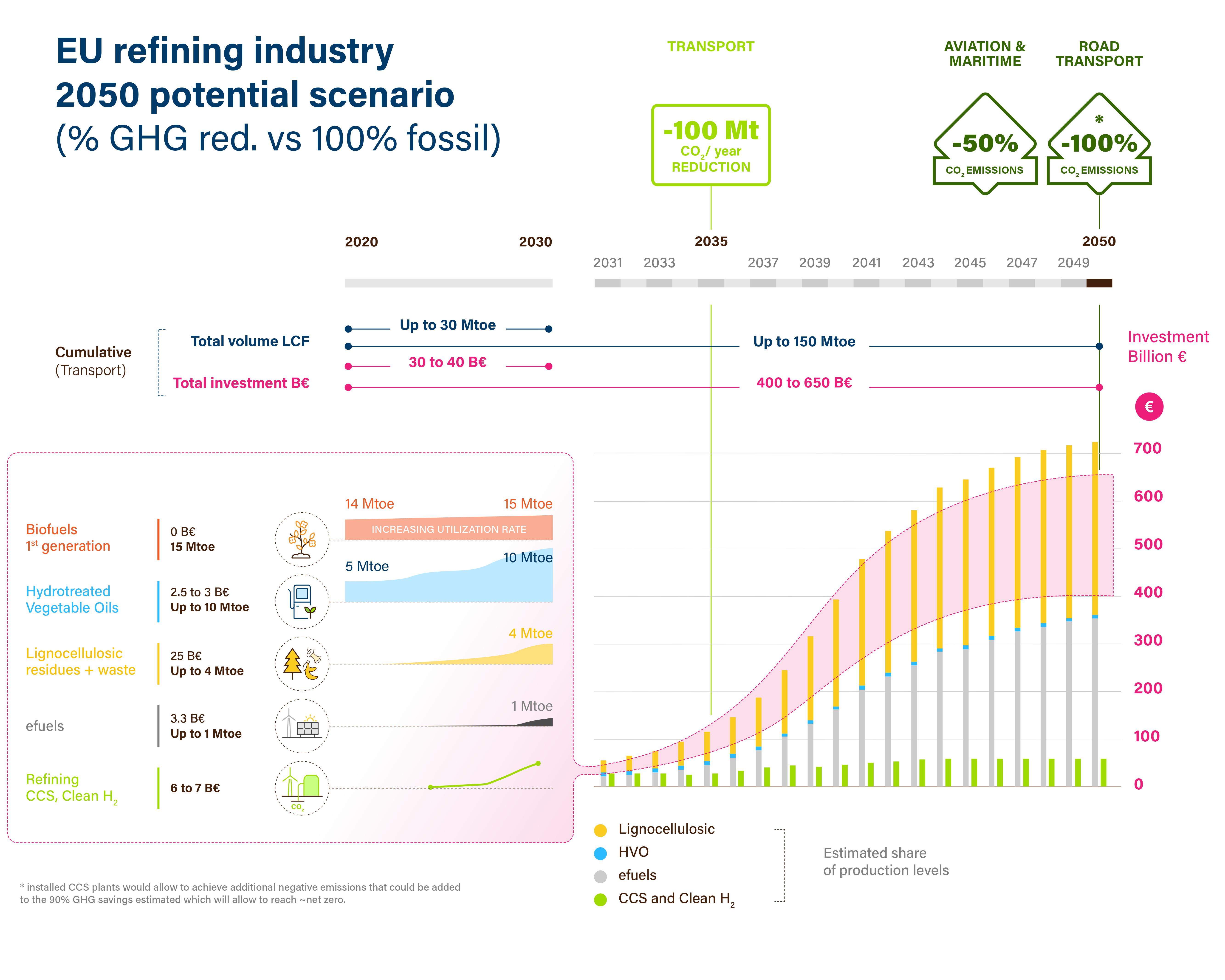

In concrete terms, based on the current technology knowledge and cost estimate, we outline a potential pathway to 2050 to develop low-carbon liquid fuels (LCLF) for road, maritime and air transport. To deliver such pathway an investment estimated between €400 to €650 billion will be needed. Major investments, in addition to those already deployed, could start in the next years, with first-of-a-kind plants at industrial scale potentially coming into operation at the latest by 2025.

Our LCLF pathway shows how a 100 Mt CO2/y reduction could be delivered in transport by 2035, equivalent to the CO2savings of 50 million Battery Electric Vehicles (BEVs) on the road, and how it could contribute to EU’s climate neutrality ambition by 2050.

LCLF will play a critical role in the energy transition and in achieving carbon neutrality in all transport modes, as the global demand for competitive liquid fuels is expected to progressively increase. Alongside electrification and hydrogen technologies, LCLF will remain essential even beyond 2050, bringing important benefits to the European economy and society.

We stand ready to enhance our collaboration with policymakers, our value chains and other partners to create the right conditions and policy framework for investments in new technologies to address the climate challenge.

By 2050, at the latest, every litre of liquid fuel for transport could be net climate neutral, enabling so the decarbonisation of aviation, maritime and road transport.

Outlined below is the pathway to enable by 2050 all new and old road transport vehicles, including hybrid or ICE, to be climate neutral, and aviation and maritime transport to achieve 50% GHG emissions reductions.

Based on the work of our industry to date, we are ready to hit the ground running. This pathway will require an estimated €30 to €40 billion investment over the next ten years and the creation of a number of biofuel and e-fuel plants that could produce up to 30 MToe/y in 2030, with the first-of-a-kind biomass-to-liquid and e-fuel plants coming into operation no later than 2025.

In concrete terms, our potential pathway includes:

By 2050, availability of 150 Mtoe of LCLF would cut over 400 Mt CO2/y. Add Carbon Capture & Storage (CCS) and the capture of emissions in biofuel production, and, in combination with electrification and hydrogen technologies, road transport reaches climate neutrality.

To meet the 2050 climate-neutrality goal, we believe Europe and its consumers need a plan where low-carbon liquid fuels and electrification/hydrogen in road transport sit side by side.

LCLF will smooth the deployment cost of electric energy distribution and fast charging infrastructure in road transport, by providing flexibility and alternative sources of low-carbon energy using mainly existing facilities.

They will reduce the pressure and cost of achieving complete fleet turnover to ensure climate neutrality, also supporting a just transition across Europe.

LCLF will give customers a choice between low-carbon technologies, ensuring that carbon neutrality is accessible to all, as LCLF will, for the foreseeable future, provide a low-cost solution compared to the alternatives.

EU citizens demand more options in the transition to carbon neutral mobility, a 2019 survey with responses from 10,000 European citizens has shown, and call on their governments to support the development of multiple clean vehicle technologies.

LCLF will provide strategic security of supply, with typically 90 days of energy supply stored within European facilities, since these fuels can be stored in exactly the same manner as fossil fuels.

Once the lead market of road transport has spearheaded the development and deployment of low-carbon technologies, the new fuels will be available for the progressive decarbonisation of aviation and shipping, enabling the groundwork for cutting up to 50% of CO2 emissions in aviation and maritime fuels by 2050.

Importantly, our pathway will also help maintain European industrial strength and jobs in the automotive sector. We see our future in a transformation of our manufacturing processes that will create European leadership in critical low-carbon technologies that will be exported around the world. Essential industrial solutions including green and blue hydrogen and CCS can also be advanced and scaled up for the benefit of many other industries.

Our proposed pathway is ambitious. The good news is our transformation has already begun.

A combination of critical technologies must be deployed in many plants across Europe to deliver LCLF at scale.

These include sustainable 1stGeneration biofuels, advanced biofuels, biomass-to-liquid, hydrogenation of vegetable oils/waste & residues, and e-fuels, to replace fossil CO2 by biogenic or recycled CO2, as well as CCS and green hydrogen applied in refineries, to reduce the carbon footprint of fuels manufacturing.

The EU refining industry is already engaged in a low-carbon transition. We are uniquely positioned to keep driving the development of these technologies, but we will not be able to achieve this alone.

Realistically, the success of our journey will also depend on investor confidence, and political vision and engagement. Notably, with a view to building the necessary market demand and start rolling out our investments in the next years, we call on EU policymakers to launch a high-level dialogue in 2020 with a view to creating a policy framework that enables:

- The creation of a market for LCLF, providing an incentive to fuels with a lower carbon footprint with respect to conventional ones. The CO2 standards in vehicles would need to factor-in the actual CO2benefits provided by LCLF compared to fossil fuels.<l/i>

- Support mechanisms for investors, both in terms of access to public and private funds, and of favourable fiscal treatment, as well as very low or zero taxation for low-carbon fuels, to facilitate fuel pricing that is both socially acceptable and able to make a business case for investments. This also implies that the EU taxonomy for sustainable activities must fully recognise the strategic importance of the transformation of the refining industry.

- The mitigation of investor risk through robust, stable, science-based sustainability criteria for all feedstock and processes, as well as ensuring the stability of the regulations impacting feedstock availability, demand of LCLF, and capital and operating costs.

Meanwhile, we are in close dialogue with multiple industries to build the necessary value chains and assets.

Agriculture, chemicals, forestry, waste and recycling, including many SMEs, will participate in these value chains. Academia, car and truck industries, aviation and maritime, and customer groups will all have a role in developing the markets with the right definitions and parameters. Civil society at large will have to be engaged through an open, transparent and fact-based dialogue.

With low-carbon liquid fuels, European refiners are ready to contribute to climate-neutral transport.

Policy principles

The EU refining industry stands ready to step up collaboration with other industries and with EU policymakers, to take bold climate action together. In order to deliver climate neutral transport by 2050, we urge EU policymakers to establish a high- level dialogue in 2020 with all concerned stakeholders to create the necessary policy framework. The following key policy principles are central to delivering our 2050 climate –neutral ambition and should serve as a starting point for discussion:

- The creation of a market for low-carbon fuels, with a significant carbon-price signal, is a prerequisite to unlock investments in low-carbon technologies and fuels. In road transport, this could be achieved through:

- Either a dedicated cap and trade mechanism on emissions from road fuels, with biogenic and recycled CO2counting as zero, with the fuel supplier as obligated party;

- Or a Well-to-Wheel (WTW) carbon intensity standard for fuels, with the fuel suppliers as obligated party and the possibility to trade credits between them.

- The CO2 standards in vehicles must be amended, whereby the actual Tank-to-Wheel (TTW) approach currently in place is corrected by taking into account the CO2 footprint of fuels. The responsibility of OEMs and of fuel suppliers should remain separate on the respective targets (in particular, OEMs will retain a TTW target), but the overall CO2 reduction in road transport should be a combination of the two. This is essential in that it would enable:

- The technology strategy of the European automotive industry to benefit from the potential to provide climate-neutral mobility with ICE-based vehicle platforms;

- Consumers to access a more accurate representation of the CO2 intensity of their mobility choices.

- All overlapping fuel policies should be reformed or simplified, such as Fuel Quality Directive (FQD)which regulates the GHG intensity of fuels brought into the market, and the Renewable Energy Directive (RED) which mandates a share of renewable content in transport fuels.

- Fuel taxation should be revised by accounting for the carbon-intensity, to incentivise investments in advanced renewable fuels. Zero or very low tax for low- carbon fuels would achieve the double objective of keeping fuel prices socially acceptable and making a business case for investments.

- Investors should be put in the best conditions to risk their capital, by:

- Ensuring regulatory stability for the economic life-time of their investment. This can be achieved by adopting robust, science-based sustainability criteria for feedstocks and processes in the first place. When, however, new regulations come into force, investments already in place must be protected from detrimental effects through grandfathering measures.

- Protecting the investments from carbon-leakage resulting from competition with less regulated non-EU industry.

- Allowing access to public and private funds for climate-related investments as well as favourable fiscal treatment.

With a clear societal and scientific case for far-reaching climate action, and taking into account the economic and social impacts of the coronavirus crisis, we respect that there will be no return to business as usual for the fuels industries. With the focus increasingly turning to recovery and new investments, we believe now is the time to start policy discussions with EU and national policy makers, and customer stakeholders to design the enabling policy framework for the deployment of these essential low-carbon fuels

John Cooper

Director General